Registration Form for

Audit Program 4.0 Live Events

Events on Audit Program 4.0 have been postponed to December. For Introduction of AP3.0, please call us at Tel: 9543-3218 / 6013-7666 to schedule a visit at your office for a personalized demonstration of the Audit Program 3.0.

We will announced the rescheduled dates for AP4.0 events in due course.

Please review the information you have provided to ensure successful registration. Please ensure you enter your CPA Practice Name and Contact Details correctly.

Please click “Register Now” when complete, and we will get in touch with you as soon as possible.

Thank you for your interest, and we look forward to seeing you at our live demonstration events.

Introducing Audit Program 4.0

Summary of AP4.0 Functions:

- Incorporated the functions of AP 3.01 into AP 4.0 to generate customized and completed audit programs using the HKICPA APM 2022 template, inclusive of client acceptance procedures, risk assessments, understanding internal controls, risk response summaries, determination of Materiality and Performance Materiality and much more!

- y-o-y fluctuation analytical reviews for each financial statement line item, and written reviews are materiality-specific, GAAP-specific and Principal-activity specific too.

- generation of completed lead-sheets / breakdowns with current and prior year numbers, and audit documentation on procedures and hyperlink cross references in each lead-sheet with direct and easy access to the respective working papers performing each procedure

- generation of sample selection planning based on imported figures, with automatic calculation of samples that are greater than PM, and sample sizes on the residual population

- generation of test of details templates for all selected financial statement line items, and automatic extraction from ledgers and completion of sampled data in our test of details templates

- generation of individual audit confirmations based on sample selection planning and debtor / creditor sub-ledgers

- generation of alternative tests for non-replied audit confirmations with automatic extraction of data from ledgers

- automatic error checking mechanisms for un-balanced BS, or PL mismatches with the statement of changes in equity and mismatches with the BS.

- automatic error checking mechanisms for mismatches between each ledger / sub-ledger and the mapped financial statements (i.e. the face) with user-friendly single-page list of all mismatches and hyperlinks to easily go to the page with the mismatch for follow-up actions

Breaking News! Run AP 4.0 in your Office!

EQC strives to provide the most cost effective solutions in your audit process. Previously we guaranteed a 2-week delivery time for the generation of completed audit programs and working paper using AP3.0 and AP4.0 respectively. To us, this is not good enough!

With the on-site installation solution, we have now reduced the turnaround time for both audit programs and working papers generation from 2 weeks down to as fast as just minutes.

There is an initial one-off set up and installation fee of HK$20,000.

The installation fee will only be charged once, even if your practice uses both AP3.0 and AP4.0.

On-Site Installation and Tutorial Service:

There is a one-off set-up and installation fee of HK$20,000.

The set-up and installation service includes:

i) Installation of AP3.0 and AP4.0 on your computer

ii) in-person tutorial and demonstration on how to use the programs to generate working papers

iii) automatic and remote update of the program(s) when we have monthly upgrades of the system.

iv) automatic calculation of credits used, and credits available for use, and transactions tracking (i.e. history of when and which engagements used the credits)

Detailed Flow of AP4.0 Functions:

Step 1: Generation of Planning Audit Programs (Automated)

AP 4.0 utilizes the latest technology of AP 3.01 to generate customized and completed audit programs. For the details on AP 3.01 and its functionalities, please visit our page at http://www.eqcadvisory.com/ap3-0

When using the Full version of AP4.0, two sets of APM are generated. One at the beginning of an audit, thus determining planning materiality ,and planning performance materiality. At this stage, the report date may not be known and total revenue, total assets and profit / loss before tax may not be finalized.

After steps 2 to 4 below, these financial statement benchmarks may be finalized, and the report date will also be finalized. A second set of APM are then generated in Step 5 of the AP4.0 Audit Process.

By simply completing the forms used in AP3.0, you will indicate to the program some of the key parameters that will be used by AP4.0 in generating the right set of APM and audit documentation for each of your audit engagements. These may include the type of financial statement line items that are present in the audit engagement, the financial reporting framework, the preliminary expected audit opinion, and the principal activities of the engagement.

Step 2: Importing the TB and Mapping with Error Checking Automation (Manual Input)

Based on the completed forms from Step 1, we will use AP4.0 to generate a balance sheet and an income statement with only the financial statement line items that have been selected in Step 1. In this balance sheet and income statement import templates, you may fill data directly from the trial balance.

For account balances, you will complete the opening balance, the total debit and total credit during the financial period, and the closing balance. For income statement line items, you will complete just the total debit and total credit during the financial period.

AP4.0 will also generate a CoA-FSLT Mapping import worksheet, in which you can easily map the accounts found in the client’s Chart of Accounts against the Financial Statements.

To facilitate this mapping process, we have built in an error-checking mechanism. where by simply a click of a button, AP4.0 would be able to check the following:

- whether there are any financial statement line items that were indicated in Step 1 of the AP4.0 Audit Process as present, but were not mapped to any accounts in the CoA-FSLT mapping.

- whether the balance sheet is not balanced

- whether there is a mismatch between the profit / loss for the year, with the movement in retained earnings

If any errors are found, an error list is generated listing out what the error is, and the to-do action to fix the error.

Step 3: Importing the Ledgers with Error Checking Automation (Manual Input)

After importing the TB, AP4.0 would generate blank ledger templates for each financial statement line item. For those financial statement line items where there is more than 1 account is mapped, a ledger import template designed for multiple accounts will be generated.

Further, by automation, AP4.0 would generate a summary indexing page that lists out all the blank ledger import templates, with hyperlinks added next to each template, allowing you to quickly jump to the specific blank template that you are working on.

To facilitate the process of importing ledgers, we have built-in an error-checking mechanism that upon a click of a button, AP4.0 would list out all the mismatches between ledgers movements and opening and closing balances against the trial balance imported in Step 2. If no mismatches are found, a clean error list is generated.

Step 4:a Year-over-Year Analytical Reviews (Automated)

Now, we have the trial balance and ledgers imported from Steps 2 and 3, AP4.0 uses automation to generate a series of working papers and audit documentation that are set out in Step 4a to Step 4f.

AP4.0 is incredibly smart. It can prepare line-by-line analytical reviews on the income statement and statement of financial position. It detects the nature of the year-over-year fluctuation, and also determines whether the fluctuation is material. For material changes, the analytical reviews would be more extensive and detailed than immaterial fluctuations.

AP4.0 is trained to apply auditor’s judgement that closely resembles to a human auditor writing analytical reviews. In addition, the fluctuation is written based on the financial reporting framework chosen!

For fluctuation analyses on revenues and cost of sales / direct costs, AP4.0 would use its knowledge regarding the client’s operating industry to customize the reasons for year-over-year fluctuation analyses.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 4b: Lead-Sheets and Breakdowns (Automated)

AP4.0 can automatically generate lead-sheets and breakdown audit schedules of each financial statement line item and extract financial information from the ledgers, trial balance and chart of accounts to achieve this.

For debtor / creditor line items, such as trade receivables, trade payables, amounts due from / (to) related parties, banks, bank loans, obligations under finance lease, etc., AP4.0 will breakdown by debtors / creditors.

For other financial statement line items, such as operating expenses, property, plant and equipment, revenues, cost of sales, etc., the generated lead-sheets will breakdown the total balance by nature, which is often segregated into multiple accounts in the books.

In each lead-sheet / breakdown schedule, AP4.0 would list out the most relevant audit procedures that should be performed, usually ranging from 3 to 6 procedures, and these are listed out directly below the breakdowns in the same worksheet.

To further facilitate your follow up and review procedures, AP4.0 would automatically generate hyperlinks and working paper cross references next to each audit procedure, so you may directly access the respective working papers on each audit procedures by clicking on the hyperlinks.

This saves your CPA Practice enormous amounts of time in cross-referencing to the audit working papers, especially when done across multiple engagements. Let automation perform the most labor-intensive work for you.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 4c: Sample Selection Planning (Automated)

AP4.0 is trained to corroborate the assertion-level risk levels determined in audit planning programs to determine the appropriate sampling risk factors, and utilize the financial figures from the imported trial balance to calculate the sample sizes.

Sample sizes are calculated for test of detail and when sampling is required for the circularization of audit confirmations.

In addition, AP4.0 is so intelligent that it dives into the imported ledgers and automatically determine the number of samples that are greater than the respective risk-based performance materiality, and determine the total value of these samples to deduce the residual population that may require additional testing.

Imagine the resources that you would save if your audit team only has to liaise with the client to provide the management accounts and ledgers, or if the affiliates that your Practice works with, prepare the accounting books directly using our import templates, and by a click of a button, the sample sizes, and working papers, for all testing and audit confirmations for all your audit engagements are generated within seconds.

Enjoy your next holiday while AP4.0 works for your Practice.

Pro-Tip: Business Strategy Proposition

Our Business Partner, Binery, has just been upgraded by Xero becoming one of the handful of Platinum Partners of Xero in Hong Kong. Platinum is the highest partnership level that Xero offers. Binery can re-sell licenses by bulk at discounted prices, and also assist to perform book-keeping functions for your clients, and the books may be directly exported to our AP4.0, creating a seamless operational flow for your clients’ accounting and auditing processes.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 4d: Test of Details and 5-Step Audit Procedures (Automated)

The capabilities of AP4.0 is similar to multiple audit seniors and audit juniors combined into one system. AP4.0 can generate test of detail templates based on the audit procedures set out in each line item’s Lead-Sheets generated in the previous steps.

However, take note that the generated test of details working papers are not simply a table for you to record sampled information. AP4.0 will write out 5 detailed audit procedures in each test of detail working paper describing how the testing should be performed. These 5 procedures are then incorporated into each test of detail working paper, allowing you to tick the procedures that were performed for each tested sample, as well as documenting the particulars of source documents.

Further, AP4.0 extracts the calculated sample sizes from the respective Sample Selection Planning papers, and dives into the ledger to extract exactly the number of samples that need to be selected. It automatically extracts the transaction amounts, voucher dates, voucher numbers and description from the ledgers and help you to fill in these data into the testing templates.

AP4.0 also segregates the samples that are greater than PM and those samples that are tested on the residual population, allowing you to cross tie the total sampled amounts to the respective totals set out in the sample selection planning sheets. As with all functions within AP4.0, this all can be done in seconds.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 4e: Audit Confirmations (Automated)

Since AP4.0 already calculates the sample sizes for test of details. How could it leave out the sample selection for audit confirmations. Using the same method, sample selection planning is automatically generated for all non-related party debtors and creditors accounts. Similar to tests of details, AP4.0 will identify the debtors and creditors accounts that have an outstanding balance in excess of the risk-based performance materiality, and automatically prepare audit confirmation for all of these samples.

In addition, AP4.0 determines if additional samples are needed on the residual population, and also prepares audit confirmations for them. AP4.0 is so intelligent that it looks through the entire ledgers for the largest samples, thus increasing your audit coverage to the maximum.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 4f: Non-Replied Audit Confirmations (Automated)

Now audit confirmations have been prepared and the client is filling in the recipients’ addresses, what is left to do? AP4.0 might as well complete the alternative tests of details assuming that none of the audit confirmations will be returned.

AP4.0 dives into the debtors’ and creditors’ ledgers and extracts the movement data in these account balances and automatically fill in alternative testing procedures templates generated for each financial statement line item where audit confirmations are circularized.

Pro-Tip: Savings in Time Costs

To give you a scope on timing, Steps 4a to 4f are all completed within seconds by ONE click of a button. It sounded a lot! With AP4.0 as your assistant, we have replaced the most manual and labor-intensive procedures with an intellectual assistant that costs less than the salary of an entry-level junior!

Just imagine the costs that you will save, the laptop, MPF, employment insurance, training costs, sick-leaves and recruitment times in handling staff turnover, the office and desk space, and of course the salaries.

Step 5: Generation of Final Audit Programs & Revisions to Sample Sizes (Automated)

If you are a current user of AP3.0, you may have come across the issue of not knowing the report dates, or the final audited sales amount when you generate the audit programs.

We have resolved this issue in AP4.0! When using the full function of AP4.0, we will grant you 1 free generation of audit programs and working papers, after you have proposed and agreed with the management on any audit adjustments, or after your client has finalized their management accounts. AP4.0 enables you to automatically re-visit planning materiality and re-visit sample selection calculation and notify you if there have been any increase in samples.

This is also a good chance if you have decided that a different audit opinion needs to be issued, as the audit completion programs can also be updated.

The free generation of Final Audit programs is only given when all features of AP4.0 are used. In essence, we are giving out a 20% discount for Practices that support our solutions fully and adopt all features of AP4.0 in their audit processes!

Note: Only limited parameters can be updated. You may not use the free generation on another audit engagement, so the financial reporting framework, principal activities, presentation currency, company name, acceptance and preparation dates, and director names, etc. cannot be changed in the second generation of audit programs.

Step 6: Issuance of Audited Financial Statements and Archive (Manual Completion)

Yes, the preparation of audited financial statements is still a manual process. As financial statements should be prepared by the clients, not the auditors. It would be strangely non-compliant if auditors are found to have a program that generates information that should have been prepared by the client!

So yes, retain your audit seniors and supervisors! You still need them to comment on the client-prepared financial statements for your review!

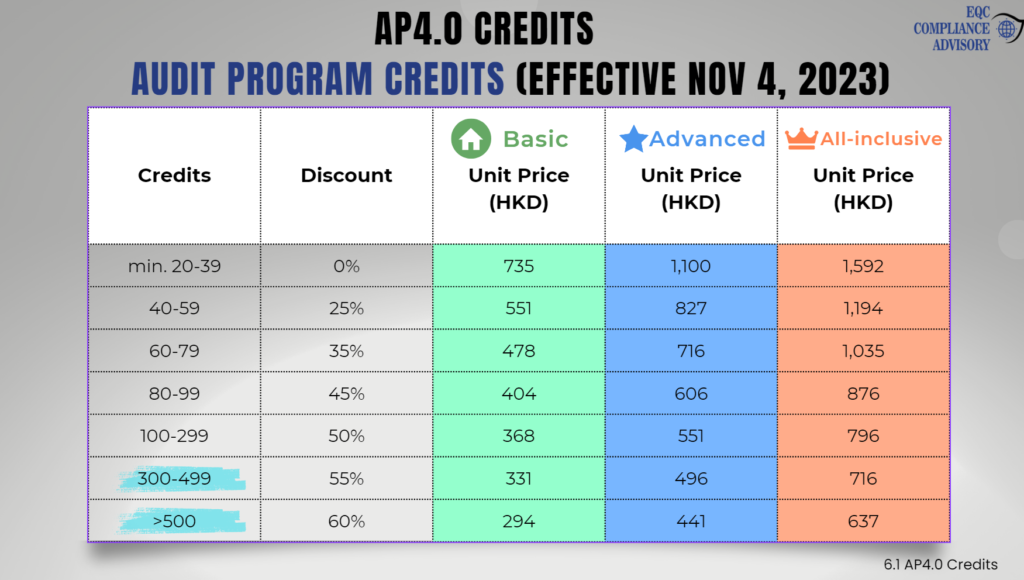

Usage of Audit Program Credits

In the use of AP 4.0 , a range of 2 to 4 credits are used in the generation of completed audit working papers for each audit engagement. subject to the functions that you would like to have for each audit engagement. All credits have a validity period of 1 year.

You have the flexibility to using the credits in whatever way you wish. For example, for an engagement with a high volume of transactions and extensive tests of details, or with significant receivables / payables balances, you may choose to use 4 credits to generate test of details, confirmations, alternatives and lead-sheets.

Whereas, for a property investment holding company, you may use only 1 credit to generate the APM, or 2 credits to generate the tests of details as well, since there would be fewer confirmations and financial statement line items for a property holding company.

Pre-Order your AP4.0 Credits Today!

We now accept pre-ordering of AP4.0 credits at a discounted price of up to 16% off when compared to the new prices becoming effective from November 4, 2023. For Pre-Ordering, we accept payment by 2 equal installments, with the balance payable within 30 days from attending our live demo events.

Breaking News:

When all functionalities of AP3.01 and AP4.0 are adopted, you only need 4 credits, at a cost as low as HK$1,320 per engagement by a purchase of 500 or more credits at Pre-Order prices, and working papers and audit programs are completed. Remember, when 4 credits are used, we allow you to generate planning and final audit programs on two separate occasions, thus allowing you to re-visit materiality, change the audit opinion, or finalize report and archive dates in the final audit programs!

These credits can be used for either the generation of just the audit programs using the latest version of AP3.01, or for the use of functions available in AP4.0.

AP4.0 Deck (Coming Soon!)

7% Monthly Price Hikes from November 4, 2023

We are implementing a 7% price hike every month in order to cover the cost of these upgrades. The first price hike was effective on 1 September, 2023. Existing clients who have purchased AP3.0 credits early will enjoy maximum value and avoid the impact of our monthly price hikes, as you will be entitled to purchase additional credits at the same price as your last purchase! If you still have not purchased any credits, we encourage you to act now. Better late, than even later!

The next monthly price hike will become effective on November 4, 20231

Save 99.9998% of your time costs now!

EQC Audit Program 3.01 and Audit Program 4.0 can help you reduce error rates , and here are 8 Pain Points that the Service may help address and we explain why your practice should use AP3.01 and AP4.0.

With the release of Audit Program 4.0 on November 20, 2023, not only will you be saving time on the completion of the APM, but you will also be saving time and money on completion of audit working papers! Lead-sheets, breakdowns, balance sheet movements, completed sample selection plannings, tests of details, confirmations, alternative tests of details for non-replied confirmations and final analytical reviews are prepared by a click of a button!

Pain Point 1: Talent Shortage

Problem 1 and Solution 1:

The talent exodus due to strict COVID-related regulations and emigration waves in recent years has left many SMEs in Hong Kong suffering from a high staff turnover rate of 20% per annum or being significantly understaffed. The audit industry is particularly affected, as many young talents are unwilling to enter this field due to its mundane, repetitive nature and long working hours.

Audit Program 3.0 and Audit Program 4.0 address the talent shortage issue by automating many mundane and repetitive tasks, making the audit process less labor-intensive and more efficient. This can help attract young talent to the industry by reducing the long working hours typically associated with audit work, making the profession more appealing and less monotonous. Automation also allows CPA firms to maintain high-quality services even with limited staffing resources.

Pain Point 2: SMP's Limited Access to Competent Staff

Problem 2 and Solution 2:

Small-and-medium sized practices (SMPs) in the audit industry face a constant challenge in recruiting competent staff, as young and experienced talents are less likely to join these firms due to the lack of career-building opportunities. This leaves SMPs with limited options for recruitment, often having to settle for inexperienced and less-educated candidates.

By streamlining the audit process and eliminating the need for extensive industry-specific knowledge, Audit Program 3.0 and Audit Program 4.0 enable SMPs to better utilize their existing staff and reduce the pressure to recruit highly experienced auditors. The automation provided by the service allows even less experienced auditors to perform high-quality audit work, bridging the competence gap and making SMPs more competitive in the market.

Pain Point 3: Labor-Intensive Audit Work

Problem 3 and Solution 3:

With new auditing standards being released almost every year, auditors have more standards to comply with, increasing the workload and resulting in labor-intensive audit work. This includes many mundane, repetitive tasks that can lead to long working hours, low profitability and recoverability on audit projects, and errors due to exhaustion and boredom when completing audit programs.

Audit Program 3.01 can tackle labor-intensive audit work by automating a significant portion of the audit process, including risk assessments, designing audit procedures, and generating completed audit programs.

While Audit Program 4.0 can generate working papers, lead-sheets, analytical reviews, sample size calculations, tests of details, confirmations and alternative tests of details.

This reduces the workload on auditors, allowing them to focus on more value-added duties and tasks that require auditor’s judgement, minimizing the risk of errors due to exhaustion and boredom, and increasing the overall efficiency and profitability of audit projects.

Pain Point 4: Industry-Specific Knowledge Gap

Problem 4 and Solution 4:

When auditing clients in unfamiliar industries, audit efficiency is often significantly reduced, as auditors lack the necessary knowledge and experience to understand the client’s industry. This can be challenging, as auditing standards require auditors to document industry-specific business processes, revenue recognition, and workflows. CPA firm owners are also faced with the difficulty of choosing to serve only specific client industries.

Audit Program 3.0 and Audit Program 4.0 help bridge the industry-specific knowledge gap by providing guidance on internal controls, revenue recognition, and cost of sales for 110 client industries. This allows auditors to quickly gain an understanding of unfamiliar industries and ensures that audit documentation is accurate and compliant with auditing standards. The service acts as a technical hub for auditors, significantly improving audit efficiency in industries where they may have limited experience.

Pain Point 5: Reviewer's Challenges

Problem 5 and Solution 5:

Reviewing completed audit programs can be a daunting task, as each set can consist of up to 300 pages of information, much of which is similar but slightly different. Reviewers face significant challenges in efficiently and effectively reviewing these audit programs prepared by junior auditors.

By automating the completion of audit programs, Audit Program 3.0 ensures consistency and compliance with auditing standards, allowing reviewers to focus their attention on high-risk areas.

Audit Program 4.0 also completes most of the working papers using programming and automation, allowing error-free working papers to be generated and reducing the workload of audit reviewers!

This reduces the time and effort required for reviewing large volumes of information, and ensures that the quality of audit programs is maintained even in lower-risk areas.

Pain Point 6: Regulatory Pressure

Problem 6 and Solution 6:

With the Accounting Financial Reporting Council (AFRC) taking over the regulatory oversight of Hong Kong CPA practices from the HKICPA, practitioners in the audit industry face increased regulatory pressure and scrutiny. Ensuring compliance with these heightened regulations is more important than ever.

Audit Program 3.0 and Audit Program 4.0 help alleviate regulatory pressure by ensuring that the audit process complies with all Hong Kong Standards on Auditing, including the latest HKSQM 1 and 2. The automation provided by the service ensures consistent compliance with these standards and reduces the risk of non-compliance, allowing CPA firms to confidently navigate the heightened regulatory environment.

Pain Point 7: New Review Procedures in AFRC Inspections

Problem 7 and Solution 7:

Under the AFRC’s new regulatory regime, there is an increased emphasis on having an effective system of quality management in place. Compliance experts speculate that the AFRC will place more focus on the timing of working paper preparation and review during practice inspections.

With Audit Program 3.0 and Audit Program 4.0, CPA firms can generate audit programs and working papers covering all substantive audit procedures ahead of time once the management accounts are received from the client, enabling auditors to only focus on the judgmental areas.

Late client adjustments and audit adjustments can be added to working papers by simply adding them to our templates, and all working papers can be updated by a click of a button!

This reduces the risk of being caught modifying working papers after archive dates, addressing the concerns around new review procedures under the AFRC’s regulatory regime.

Pain Point 8: Limitation of Traditional Templates

Problem 8 and Solution 8:

Traditional templates provided by CPA firms or consultancy firms for auditors to use in completing audit engagements have their limitations. Auditors may choose the wrong templates or omit important papers, and they may also lack the knowledge to properly complete or customize these templates.

Audit Program 3.0 and Audit Program 4.0 go beyond traditional templates by not only providing the template but also completing illustrative model answers specific to each audit engagement. Working papers are completed based on the imported financial information, and templates used for importing financial information are so user friendly that even untrained client’s accounting team can complete them.

This ensures that the right templates are used and that auditors know how to customize them to suit the particular circumstances of the engagement. The service eliminates the limitations of traditional templates, allowing CPA firms to streamline their audit process and maintain compliance with the latest accounting and auditing standards.

Six More Reasons to Use AP 3.0 and AP 4.0

i. Resolves the Most Common Practice Review Findings

Over the past 3 years, EQC has been constantly improving our documentation in addressing common practice review findings, and we can confidently confirm that our Audit Program 3.0 can effectively address TEN of the most prevalent audit deficiencies that are commonly found in audit programs across the entire SMP industry.

-

- Lack of understanding of the internal controls on key business processes.

-

- Lack of assertion-level, financial statement-level, inherent and control risk assessments.

-

- Lack of fraud risk considerations and inadequate procedures on management override of controls.

-

- Lack of assessments and evaluation of key accounting estimates.

-

- Lack of customized audit procedures tailored for your specific industry, when applying a specific financial reporting framework, such as SME-FRS, HKFRS for PE, or HKFRS.

-

- Lack of considerations of the impact of new accounting standards on opening balance and current year financial statements.

-

- Lack of documentation on work done on going concern considerations.

-

- Lack of documentation to justify the use of a specific type of audit opinion, such as material uncertainty paragraph, qualified opinion, adverse opinion or disclaimer of opinion.

-

- Lack of considerations of prior year’s modified audit opinion, and how it affects your client acceptance and engagement continuance procedures.

- Lack of audit scoping for significant components of group audits, and insufficient documentation on the proper determination of group and component materiality.

- Lack of extensive analytical review performed to corroborate understanding obtained throughout the audit. These analytical reviews should include explanations of year-over-year fluctuations that go beyond explaining impact of socio-economic trends.

- Lack of a systematic method in determining extend of audit work through a sampling method that is consistent with audit planning’s risk-based assessment

- Lack of documentation of particulars of tests of details, often with just ticks with no documentation on the selected journal voucher and particulars that were examined.

- Lack of audit confirmations sent out to debtors and creditors

- Lack of audit evidence on alternative procedures performed for any non-replied audit confirmations

- Lack of step-by-step audit procedures documented on each test of detail

- Inconsistency between working papers after late audit adjustments are taken up by the management of the client.

ii. Fastest Turnaround Delivery in the Market

Now you are familiar with the problems it resolves, you would probably be wondering if we have the manpower the complete so many audit programs. We adopt Artificial Intelligence, Machine Learning and Complex coding that we have internally developed in the delivery of completed audit programs using Audit Program 3.0 and completed working papers using Audit Program 4.0.

We proudly guarantee a 2-week turnaround time. With EQC, it is no longer a dream that audit documentation that complies with Auditing Standards, can be completed and archived within 60 days from your audit report date. What worries would you still have over practice reviews if all your audit engagements have sufficient documentation, and all your audit files are created AND archived before the archive deadline?

iii. Save 99.9998% of your Time Costs

Through our determination on digital transformation, we have been able to lower the cost to levels significantly below the equivalent time-cost of a typical audit junior.

The lowest cost of a qualified auditor who can write effective audit documentation on internal controls, revenue recognition processes, evaluation of key accounting estimates, etc. would cost around HK$30,000 per month before annual leaves, bonuses and benefits. To write one of these documentation, it may take 20-30 minutes, equivalent to a cost of HK$57 – 85.

Our Advanced version (not the strongest version) of the program provides in excess of 22,500,000 permutations of customized model answers, at a cost as low as HK$450 per completed audit program for your audit engagement. The permutations of Audit Program 4.0 is further raised to billions, effectively reducing the cost to infinitely close to zero per written answer., effectively saving up to 99.9999% of your time costs.

The generation of completed working papers will merely cost 2 to 3 more credits, and the whole audit can be completed on a budget of under HK$2,000 (subject to monthly price hikes, this was written in October 2023).

You no longer have to pay hefty upfront costs to buy working paper templates or other audit systems, which would still require an additional budget for training and audit inefficiencies, and payments of salaries, and more often than not, these trained staff may “jump-ship” to other firms after a short period of employment. Imagine all the recurring fixed costs that you can start saving today.

iv. Technology Helps to Eliminate Human Errors

Human mistakes arising from carelessness is always inevitable. If you have previously purchased / encountered working paper templates available in the market, you would realize that it would almost be an impossible feat to digest the 1000-page long audit practice manual to ensure that the documented procedures have indeed been carried out in your working paper files.

Any inconsistencies between your firm’s audit practice manual and the archived working papers would be undisputable indicator of weakness in the firm’s engagement performance procedures.

Our technological-based Audit Program 3.0 and Audit Program 4.0 help to eliminate any inconsistencies between the 200-page programs, your audit schedules sample size calculations, your working papers, and your audited financial statements, which would also significantly reduce your costs in file reviews. Your time can thus be re-invested into areas that commercially matter to your business.

v. Over 1 billion permutations

Audit Program 4.0 offers the following options when generated the illustrative completed audit program!

1. Financial Reporting Framework: 3 choices

2. Risk Levels: 2 choices

3. Financial Statement Line Items: 96 choices

4. Principal Activities: 115 choices

5. Accounting Estimates: 27 choices

6. Modified Audit Opinions: 25 choices

7. Line-by-line Analytical Reviews that can detect whether the line item increased / decreased, and whether the decrease is material when compared to PM, and thus giving a explanation of the fluctuation that is GAAP and Principal activity specific.

8. Tests of details directly extract relevant data from the ledgers

9. Confirmations to drafted and prepared based on debtor / creditor ledgers

10. Alternative tests of details extract invoice issuing and settlement data from the ledgers.

There are over 1 billion possible permutations for your program with these parameters and choices. That is real customization at a very low cost!

vi. Use for Consultancy Services, Internal Training and More!

Who said that the Audit Program 3.0 can only be used for your practice’s audit and assurance services?

Imagine your client engaged you for internal control consultancy prior to a planned IPO, and your client operates in a specific industry that you are unfamiliar with. All you have do is, use 1 of your purchased credits to generate an Audit Program specific to your client’s industry, and you will have pre-written internal controls specific to that industry!

Imagine your client needs to improve their internal controls to address previous financial statement level or fraud risks, and needs to write a comprehensive internal control manual covering all business processes of the company, from sales, marketing, human resources, disbursement claims, management of investment properties, property plant and equipment, making investment decisions, managing loans, and registering patents and trademarks. Yes! We cover the internal controls of all these processes and much more!

Imagine you have a network of potential clients in regulated industries, such SFO regulated, brokers regulated under Insurance Ordinance, or Solicitors’ Firms under the Accountants’ Reports Rules, and Law Society of Hong Kong. Now you can generate audit programs for each of these industries, and have customized list of audit procedures when preparing the compliance reports or accountants report of these engagements, significantly lowering your regulatory risks!

Imagine you are going through a AFRC inspection, and you are asked to elevate your practice’s audit quality in auditing specific account balances, or when applying specific new accounting or auditing standards. Now with Audit Program 3.0, you can create your own in-house training materials using our generated model answers, and use these training decks as evidence of remedial actions taken by your practice!